Remember when term deposit interest rates meant something

Cash has and always will, play a key role as a source of security and liquidity in our lives. Cash is needed to provide for short-term goals and emergencies, and is supported by a Government Guarantee of up to $250,000 per bank or ADI (Authorised Deposit Taking Institution).

There has traditionally been another purpose of cash for savers – a source of interest income without the associated anxiety and stress of capital volatility and risk. The Peace of Mind factor!

At The Peak Partnership Wealth Design Solutions we have always been cognisant of this intangible benefit for our clients, especially leading up to and during retirement. Holding an appropriate level of savings or term deposit accounts in a diversified retirement portfolio (the peace of mind allocation) allows an investor to have the right mindset and time horizon for the balance of their investments (the productive allocation).

On the flip-side, holding too much cash has always been a risk for longer-term capital preservation. Today, with global and domestic interest rates approaching 0%, the risk/return trade-off has definitely skewed away from holding too much in cash or term deposits. Whilst there is little short-term risk in doing so, the long-term risk can be very high as inflation and the returns from other assets deflate the real value of your cash.

Why are interest rates so low?

In Australia, low interest rates have been engineered by the Reserve Bank of Australia (RBA) to stimulate economic activity and inflation.

Pre COVID-19, there may have been an expectation that interest rate settings may gradually increase again over time, giving savers a ray of light. However, the pandemic's impact on global economies and the need to provide confidence to businesses and home buyers to borrow will likely lead to rates being low for longer. Recent commentary by central banks support this 'lower for longer' interest rate theme.

By eroding the return on risk-free investments, households and businesses are encouraged to pursue higher returning opportunities. Now, for pre and post retirees in particular, the critical thing to remember is that as you invest higher up the return spectrum, the higher the level of risk.

The good news is that there are ways to generate a more tangible return outcome than cash, without venturing too far up the risk scale.

Bonds and diversification.

People feel very secure “lending” their hard earned money to a bank. Indeed, it took a Global Financial Crisis (September 2007 to March 2009) to highlight the fact that bank deposits (essentially lending your money to a bank) is not risk free!

To restore confidence in the banking and financial system, governments around the world started to guarantee bank deposits. This guarantee is still in place globally and in Australia today. The traditional way to generate a risk-free return though, is to lend your money to the government, investing in their bonds through to maturity.

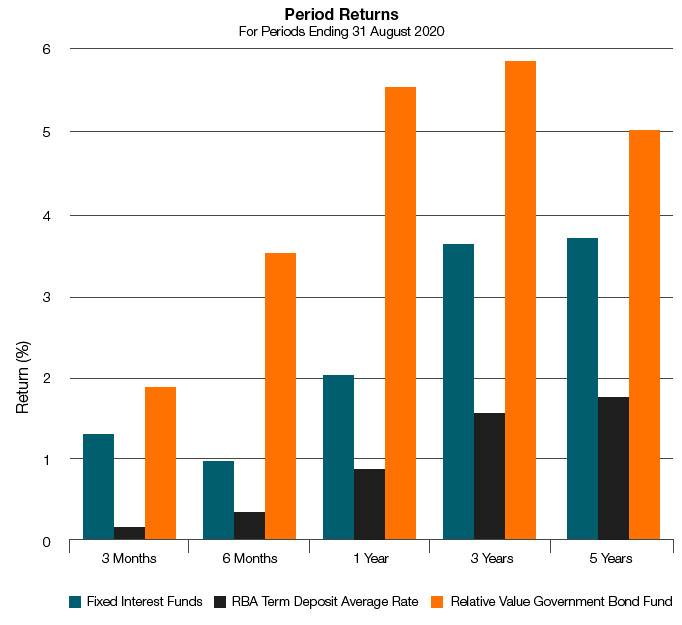

Given the low risk outcome, the return is also very low in the Government Bond market, however there are ways that astute fund managers can take advantage of the low-risk nature of the Government Bond market to generate a more tangible return outcome for investors (see period returns for Relative Value Fund in chart below).

Likewise, the Corporate Bond market provides the ability to generate a solid return without compromising investors overall risk position too much.

Large companies generally raise capital for their business in one of two ways, by issuing shares or bonds. As a shareholder, you become a part-owner of the company and share in the fortunes or misfortunes of the business over time. Shares are fantastic long-term investments, however you need to have the right mindset and time horizon in mind to mitigate the inherent risks.

As a bond holder, your return is more stable in the form of an interest payment (known as a coupon) every six months until the maturity of the bond, as long as the company itself doesn’t default. The key here is to diversify away as much credit (default) risk as possible and focus on Investment Grade or above underlying bond issuers.

These offer a lower risk, having been assessed as having a strong capacity to meet their financial commitments. Now, because you are not rewarded by having a concentrated exposure, the more underlying bond issuers in your portfolio the better. Importantly, this can easily be achieved with a well-managed, diversified bond fund. In fact, there are high quality Conservative funds that can provide you with diversified exposure to shares and bonds, whilst moderating volatility and risk.

One call could spark some interest.

Regardless of interest rates, we are the first to stress the importance of maintaining adequate cash reserves however it is now very timely to consider alternative sources of low risk return. Be wary of high interest, single issuer offerings or high interest mortgage trusts as the high rates are usually reflective of the additional risk these investments hold.

If you find that your bank continually offers very low rates on your term deposits, feel free to contact me and my team at The Peak Partnership Wealth Design Solutions. We can help you design an appropriate plan, cash allocation and investment strategy to deal with the current low interest rate environment.