Quarterly Update: DECember 2025

Here are the key points from our Market and Economic Update for the December quarter 2025:

- International equities rose while Australian equities struggled: International equities finished the year strongly as investors focused on positive headlines. Late in the year, market leadership broadened to sectors that had previously lagged amid the dominance of large cap technology. In contrast, Australian equities weakened following the re emergence of inflation pressures.

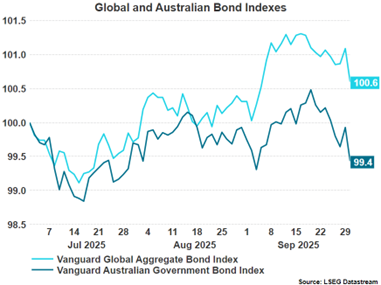

- International bond yields fell, while Australian yields rose: Positive economic data and easing inflation prompted investors to price in further rate cuts from central banks globally, placing downward pressure on international bond yields. In Australia, higher than expected inflation delayed the expected path of RBA rate cuts, resulting in rising local yields.

- USD and AUD appreciation: The US dollar appreciated against most major currencies, rising through the early part of the quarter before pulling back in December as expectations for additional rate cuts increased. The Australian dollar also strengthened as persistent inflation concerns led investors to price in higher domestic interest rates for longer.